Couch to £5k: making your savings pay

According to the Building Societies Association, one-third (33%) of people are putting money aside to cover unexpected costs – a ‘rainy day’ emergency fund.

Money Matters | October 2024

Autumn is here – in all its squirreling, puddling and breezy glory. And, with UK savings week recently behind us, now is a great time to warm-up your savings and start planning for a tropical getaway.

Another ‘rainy day’?

Well, according to the Building Societies Association, one-third (33%) of people are putting money aside to cover unexpected costs – a ‘rainy day’ emergency fund. And, around one in four are saving for holidays (26%) and for later life (25%).

Taking the first financial step

Like the post-lockdown Couch to 5K craze, building your savings can start with small, manageable steps that can lead to impressive results.

Whether you’re a novice or savvy saver, we believe it’s possible to make £5,000 interest from existing savings of £60,000, without having to move banks (or even off the couch), and we’d love to show you how.

Ready to get started? Read on…

Step 1. Set clear financial goals

The first step in any fitness programme is to set clear, achievable goals. The goal we’ll explore here is, for example, to earn £5,000 interest from £60,000 of savings within two years.

- Goal: £5,000

- Total savings: £60,000

- Timeframe: Two years

Step 2. Cash (ISA) is king

Cash ISAs offer tax-free interest on up to £20,000 each tax year.

A secure and stress-free way to keep more pounds in your pocket, it’s a logical place to start saving for those who are eligible.

Example:

- We’ll open an ISA fixed term account (2 years fixed)

- Pay-in £10,000 at 4.25% AER tax-free

- Earn an estimated £868 in 2 years.

Step 3: The rainy-day fund

It’s important to keep some of your savings handy to dip into should something unexpected happen – the boiler goes, the car needs major work, the tax bill is higher than expected… allowing life to carry on with less worries. These are variable accounts and the interest rate can decrease as well as increase.

Example:

- We’ll open an easy access savings account

- Pay-in £10,000 at 4.65% AER

- Earn an estimated £952 in 2 years (assuming the rate doesn’t change).

Step 4. Fix what you don’t need

Fixed rate savings accounts are a great option for safely securing your cash away and knowing exactly how much you’ll get in the 2 years.

Only put aside money you definitely will not need during the two years because you won’t be able to withdraw them until the end of the term.

Remember, don’t put all your eggs in one basket – find the right balance for you.

Example, where we’ll invest £33,000 in a range of fixed term accounts:

- Open a new 1 year fixed term account

- Pay-in £3,000 at 4.60% AER

- Earn roughly £138 in interest

- After the year, at maturity, move this into the easy access account, and earn an extra £146.

- Open a new 18 month fixed term account

- Pay-in £10,000 at 4.51% AER

- Earn roughly £681 in interest

- After 18 months, at maturity, move this into the easy access account, and earn an extra £248.

- Open a new 2 year fixed term account

- Pay-in £20,000 at 4.51% AER

- Earn roughly £1,845 by the end of the term.

With these examples, you could earn an estimated £3,013 in 2 years.

Step 5: Start a regular savings habit

Start paying a stretching (but affordable) amount into your easy access account monthly for the next two years (set it up as a regular payment so you can forget about it). While this won’t yield a huge return, you’ll be surprised how quickly it builds and will always be easily accessible if you need it.

- Let’s say we’ll save £300 a month

- Pay this into the easy access account we opened earlier

- Earn roughly £351 in 2 years (plus you’d have squirreled away an extra £7,200!).

Pro tip: Our online portal makes it quick and easy to apply for extra easy access accounts and rename them depending on your financial goals. Making it really easy to stay laser-focused on that dream holiday.

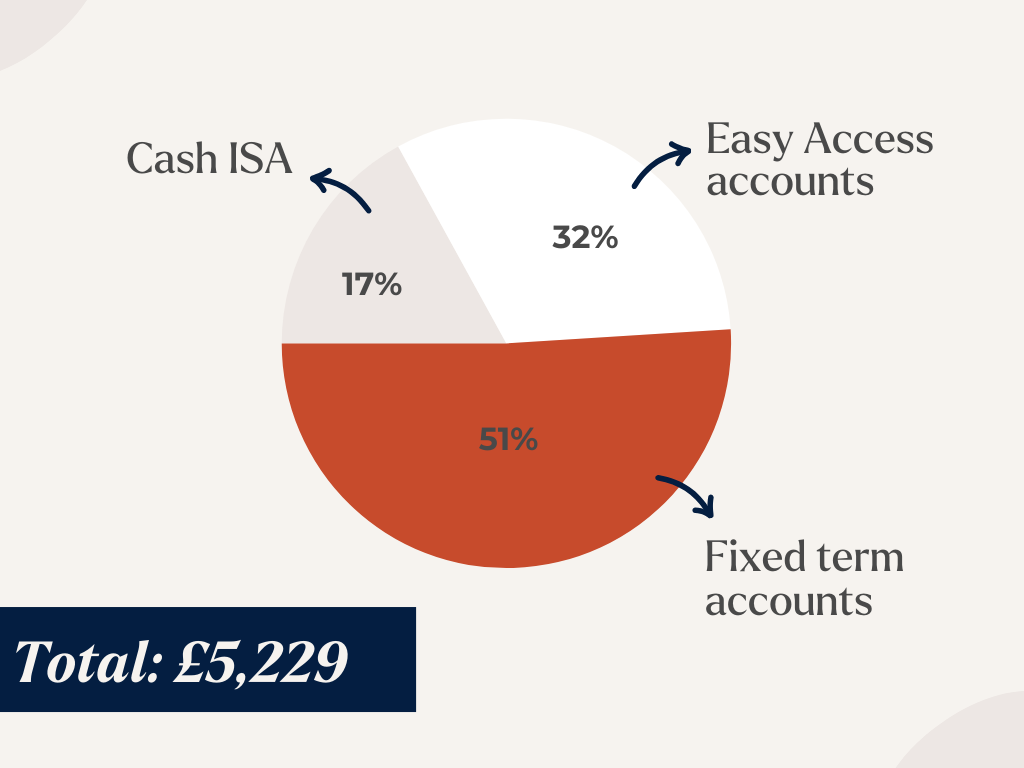

The results are in…

In our examples, we earned £5,229 total interest pre-tax (from our couch).

Find a balance of account types that work for you, and it’s clear that savings can work hard for you, too.

So, let’s start saving.

HTB doesn’t provide financial advice. The examples are for illustrative purposes only and this article should not be seen as financial advice.

Everyone’s savings and tax position are different. Individuals are responsible for declaring any interest earned on their savings by completing and summitting a tax return.

Learn more about HTB’s savings accounts here.

We offer solutions for businesses, individuals and intermediaries.